FBR Can No Longer Assume Your Bank Inflows are Income—But You Should Still Be Careful

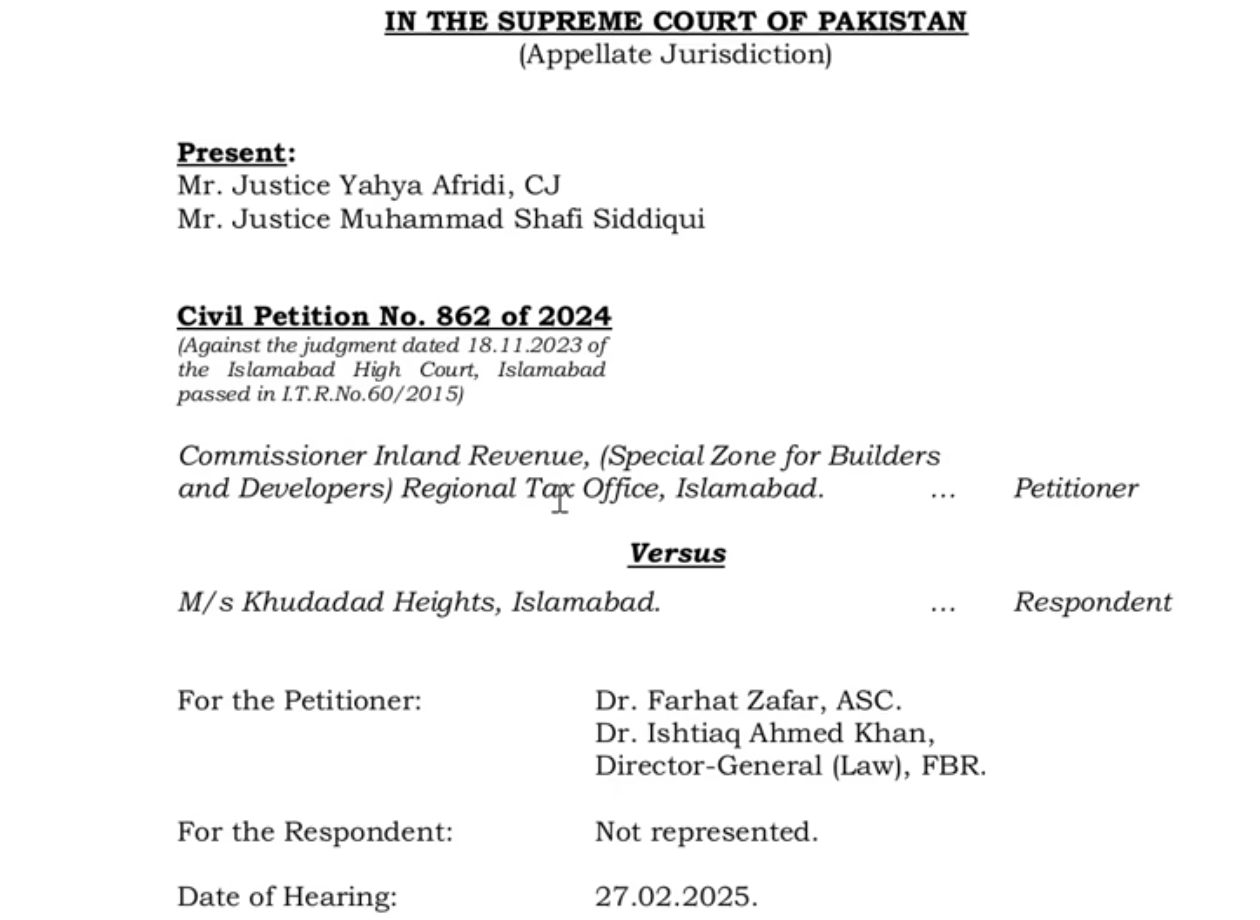

In a landmark development for taxpayers across Pakistan, the Supreme Court has ruled that the Federal Board of Revenue (FBR) cannot treat the total credit balance in a bank account as taxable income without specific verification. The judgment strikes a blow against the revenue body’s growing reliance on automated notices, declaring that bank statements alone are insufficient to establish income liability.

The ruling comes as a significant relief for salaried individuals and business owners who have increasingly found themselves at the receiving end of tax notices based on gross bank inflows.

Court Rules: Credits Are Not De Facto Income

The Supreme Court’s order addresses a long-standing grievance where tax officers assumed that every deposit into a taxpayer’s account—whether a loan, a gift, or a temporary transfer—constituted earnings.

In its judgment, the Court observed that a “bank statement alone does not necessarily reveal the defined income of a taxpayer.” The verdict clarified that credit entries often reflect non-income transactions, such as the repayment of loans or family transfers. The Court dismissed the department’s appeal, asserting that the FBR must examine the “nature and source” of funds before calculating tax liability, rather than simply applying a tax rate to the total money that passed through an account.

The “Total Credit” Trap

Tax experts warn that the disconnect between actual income and bank activity has become a primary trigger for audits.

“The FBR’s automated systems often pick up the total credit side of a bank statement and flag it as concealed income,” explained Faheem Mehboob, a tax expert and commentator, in a detailed analysis of the order. “If a taxpayer takes a loan of 1 million rupees and repays it later, the bank statement shows a credit. The FBR sees this as income, even though the net financial impact on the taxpayer is zero.”

Mehboob noted that while corporations with legal teams can easily challenge these assumptions, the average taxpayer often struggles to navigate the complex appeals process. “An officer might not understand that a debit and credit entry cancels out. They see the inflow and demand tax,” he noted.

Risks Remain for 2026

Despite the legal victory, experts are advising caution heading into the 2026 tax year. The FBR’s use of artificial intelligence and automated data matching means that “noisy” bank statements are still likely to trigger audit notices, forcing taxpayers into a lengthy process to prove their innocence.

“Even with this judgment, if your declared salary is 2 million but your bank credits show 10 million due to temporary transfers or loans, the system will flag you,” Mehboob warned.

Taxpayers are being urged to “clean up” their banking habits by:

-

Limiting non-essential transactions: avoiding the use of personal accounts for third-party transfers.

-

Segregating funds: keeping business and personal finances distinct.

-

Documenting loans: maintaining written evidence for any temporary financial assistance received from friends or family.

While the Supreme Court has legally burdened the FBR with proving that a deposit is income, the burden of avoiding the initial scrutiny still falls on the taxpayer. As the new tax year approaches, the message from legal experts is clear: relying on the courts to fix a tax assessment is possible, but avoiding the notice through prudent banking is preferable.